The Challenge – to change an Industry

The UK mortgage industry, valued at £286.7 billion in new lending annually (UK Finance, 2024), faces a critical paradox: whilst mortgage products have grown increasingly complex, the tools available to advisors remain stubbornly antiquated. Mortgage advisors spend 90% of their time on administrative tasks—data entry, document parsing, compliance paperwork—leaving only 10% for what they do best: providing expert, tailored advice to clients navigating one of life’s most significant financial decisions.

JammJar emerged from a simple but powerful question: What if we could invert that ratio?

My Role: Translating vision into reality

Between July 2024 and April 2025, I served as Lead Product Designer and UX Consultant for JammJar, a venture founded by an experienced mortgage advisor determined to transform his industry. My mandate was to take a raw concept—leveraging AI to revolutionise mortgage advisory—and translate it into a tangible, usable, and desirable digital service that could compete with established players whilst carving out a distinctive position in the market.

This was a quintessential 0-1 project: no existing product, no design language, no defined user journeys. Just deep domain expertise from the founder, emerging AI capabilities, and an opportunity to reimagine an entire professional workflow.

Understanding the Territory: Immersion and Discovery

Ethnographic Research in the Field

To understand the mortgage advisory landscape, I conducted field research:

- Site visits to active mortgage advisory firms across the UK, observing advisors in their natural working environment

- Contextual interviews with 8 practicing mortgage advisors, documenting their workflows, pain points, and workarounds

- Shadowing sessions to understand the granular details of fact-finding, document processing, and client interactions

- Attendance at industry events including mortgage advisor conferences and Financial Conduct Authority (FCA) compliance workshops

The reality behind the statistics

What emerged was a portrait of an industry trapped between competing demands:

Time allocation reality:

- 50%+ of advisor time: Manual data entry from paper forms and PDFs

- 15-20%: Chasing missing documentation from clients

- 10-15%: Compliance and audit trail maintenance

- 5-10%: Actual mortgage product research and comparison

- <10%: Face-to-face advisory conversations with clients

The hidden costs: One advisor candidly shared: “I became a mortgage advisor to help people achieve their dream of homeownership. Instead, I spend my days typing numbers into spreadsheets and reading Key Features Illustrations line by line. The job I imagined doing occupies maybe 2 hours of my week.”

Competitive landscape analysis

I conducted detailed competitor analysis of emerging digital mortgage platforms including Habito, Tembo, and Better.com, alongside established players like Mortgage Advice Bureau’s digital offerings. The analysis revealed three distinct strategic positions:

- Direct-to-Consumer Automation (Habito, Better): Removing the advisor entirely, optimising for speed and cost

- Advisor Augmentation Tools (existing CRM systems): Digitising traditional workflows without reimagining them

- Hybrid Human-AI Advisory (our opportunity): Preserving expert judgment whilst eliminating administrative burden

Our strategic differentiation: JammJar would position itself in the emerging third category: using AI not to replace advisors, but to liberate them to focus on high-value advisory work. We termed this “AI-augmented expertise”—where machine learning handles pattern recognition, document parsing, and compliance checking, whilst human advisors provide judgment, empathy, and tailored guidance.

Regulatory deep dive

The UK mortgage industry operates under stringent FCA regulation. I immersed myself in:

- FCA Conduct of Business Sourcebook (COBS) requirements for mortgage advice

- GDPR implications for handling sensitive financial data

- Consumer Duty regulations (implemented 2023) requiring demonstrable good outcomes

- Suitability Report requirements and audit trail documentation

This regulatory landscape wasn’t a constraint—it was an opportunity. Properly implemented, AI could improve compliance by ensuring consistent documentation, complete fact-finding, and auditable decision-making processes.

Defining the Problem: synthesis and insight

Jobs to Be Done Framework

I employed the Jobs to Be Done (JTBD) framework to move beyond surface-level feature requests to underlying motivations:

Mortgage Advisor JTBD:

- Primary Job: “Help my clients secure the most suitable mortgage for their circumstances whilst building a sustainable advisory practice”

- Functional Jobs: Compare mortgage products, complete fact-finds, produce compliance documentation, maintain client relationships

- Emotional Jobs: Feel confident in recommendations, reduce anxiety about regulatory compliance, experience professional satisfaction

- Social Jobs: Build reputation, receive referrals, be seen as an expert trusted advisor

Mortgage Applicant JTBD:

- Primary Job: “Navigate the mortgage process with confidence that I’m making informed decisions and won’t be rejected”

- Functional Jobs: Understand eligibility, compare options, provide required information, complete application

- Emotional Jobs: Reduce anxiety about rejection, feel in control of the process, trust that I’m getting unbiased advice

- Social Jobs: Achieve homeownership milestone, make financially responsible decisions

The Core Insight

Traditional mortgage advisory software optimises for transaction processing. But advisors don’t want to process transactions—they want to provide excellent advice efficiently. Meanwhile, mortgage applicants don’t want to be processed—they want to be guided through a complex, high-stakes decision.

The opportunity: Design a system where AI handles the transactional mechanics, freeing both advisors and clients to focus on understanding, decision-making, and relationship-building.

Navigating constraints: Strategic trade-offs

The Build vs. Complexity Matrix

Early in the project, we faced a critical decision about scope. The comprehensive vision included:

- Advisor-facing case management platform

- Client-facing fact-find interface

- AI-powered document parsing

- Mortgage product comparison engine

- Suitability report generation

- Compliance audit trail system

- Integration with lender APIs

- Mobile applications for advisors and clients

The Trade-off Decision: Given development resources and time-to-market considerations, we prioritised:

- Phase 1 (Launch): Advisor platform with AI document parsing and fact-find management

- Phase 2: Client-facing fact-find interface

- Phase 3: Advanced analytics and lender API integration

Rationale: Advisors are the gatekeepers and paying customers. Solving their most acute pain point—document processing and data entry—would create immediate value and word-of-mouth growth, even if the client experience initially remained largely unchanged.

The Path not taken: We considered a client-first approach (building a Habito-style consumer interface) but rejected it because:

- Advisors would see us as a threat rather than a tool

- It wouldn’t leverage the founder’s advisor network for initial distribution

- It would put us in direct competition with well-funded consumer platforms

This decision shaped the entire product architecture and go-to-market strategy.

The AI Transparency Dilemma

A persistent debate centred on how visible to make AI processing:

- Option A: Hide the AI Present results as if they came directly from advisor input, making the system feel like a faster version of existing tools.

- Option B: Expose the AI Show confidence scores, highlight where AI made inferences, allow advisors to see the “working out”.

Our Approach: Transparent Augmentation We chose Option B with careful design treatment. Advisors needed to trust the system, and trust requires visibility. However, we designed the interface so AI suggestions felt like collaborative input from an intelligent assistant rather than autonomous decision-making requiring review.

Design Pattern: When JammJar’s AI (at that time, personified as “Marvin” but it is now unnamed) parsed a document, it would:

- Highlight extracted data fields

- Show confidence level (high/medium/low)

- Provide “Show me” links to source document locations

- Allow one-click acceptance or manual override

This pattern became central to the entire product: AI proposes, human disposes, but AI handles the mechanics.

The Mobile Question

Site visits revealed advisors working in three contexts:

- Office desk (desktop)

- Client homes (laptop + tablet)

- Travelling between appointments (mobile)

The Trade-off: A truly responsive design accommodating all contexts would add 40-60% to development time. We chose to:

- Prioritise desktop for deep work (document review, suitability reports)

- Ensure tablet compatibility for client meetings (fact-find collaboration)

- Accept degraded mobile experience initially, with targeted mobile features (call logging, quick notes) in Phase 2

Validation: Post-launch research confirmed this prioritisation; advisors primarily wanted to do “real work” on larger screens, using mobile only for lightweight updates.

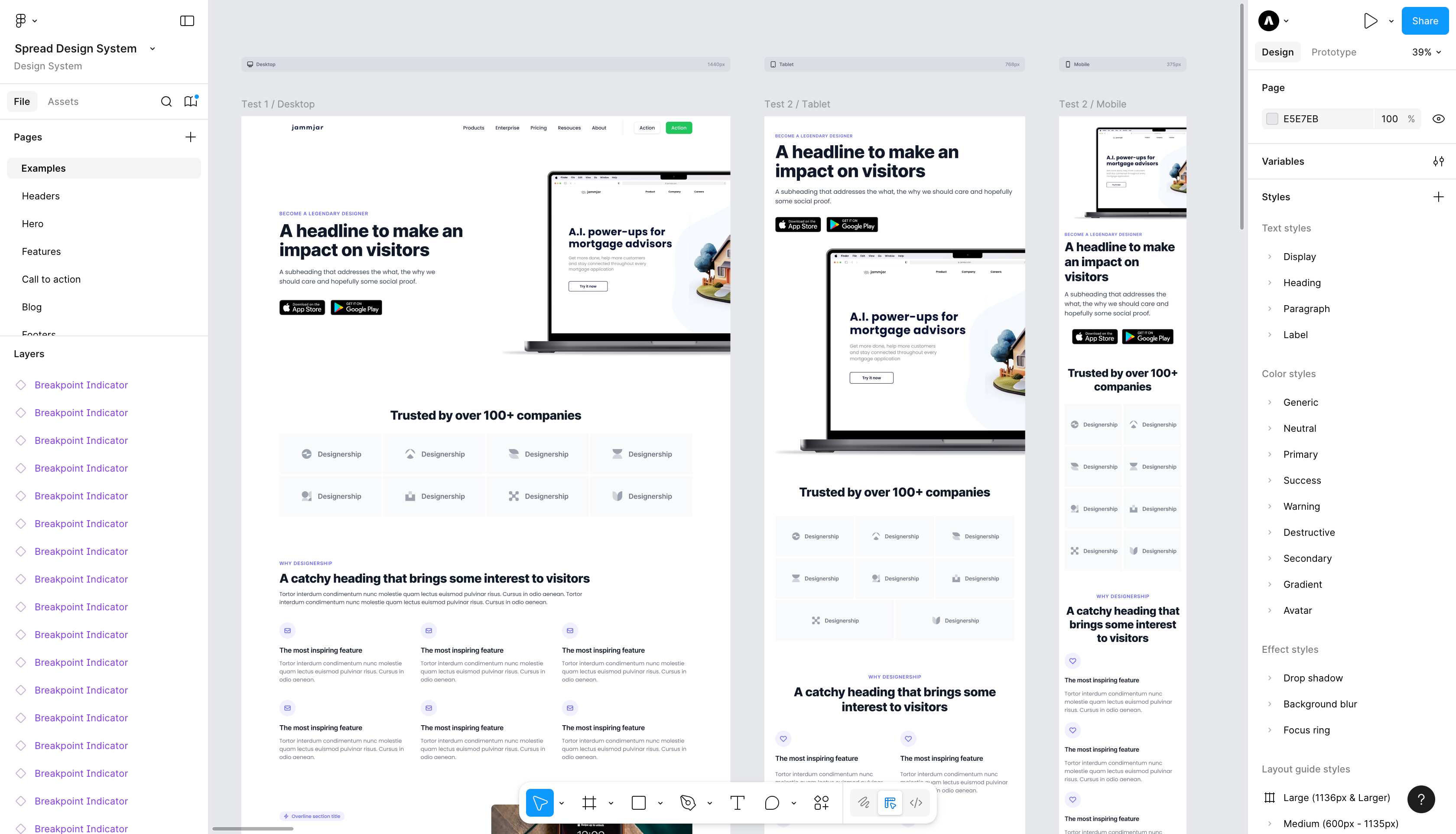

Building the Foundation: Spread Design System

Before designing any product screens, I recognised we needed a robust foundation. Drawing on my experience building design systems at Amazon, I created Spread—a comprehensive design system that would enable rapid, consistent product development.

Why “Spread”?

The name emerged from a simple association: jam spreads across toast, and this design system would spread across all JammJar products and interfaces. (The founder and I briefly debated “Spreadd” with two d’s, but clarity won over cleverness.)

System Architecture

Spread comprised:

1. Design Tokens

- Colour palette (primary, secondary, semantic colours)

- Typography scale (6 levels)

- Spacing scale (4px base unit, geometric progression)

- Elevation and shadow system

- Border radius and line weight standards

2. Component Library

- 47 base components (buttons, inputs, cards, modals, navigation)

- 12 composition patterns (forms, tables, dashboards, document viewers)

- 8 page templates (dashboard, detail view, list view, settings)

3. Configurability Layer The system’s power lay in its configurability. Key variables could be updated centrally:

- Brand colours (primary and secondary)

- Logo and brand marks

- Iconography style

- Illustration treatment

- Photography treatment

This meant the entire application’s visual identity could be updated in hours, not weeks—critical for a venture still exploring its brand identity.

The Economic Argument

At Amazon, design systems of comparable scope required:

- 3-6 months of dedicated design team time, or

- £30,000+ agency engagement

By leveraging patterns from six years of experience, I compressed this timeline to approximately three weeks of intensive work. The founder valued this contribution not just for time saved, but for the optionality it created: we could experiment with different brand positions without rebuilding the product each time.

Designing the Experience: From Concept to Prototype

High-Fidelity Prototyping Philosophy

I employed high-fidelity, clickable prototypes from the outset. This decision was deliberate:

Why High-Fi Early?

- Developer handoff: The development team could inspect actual styles, spacing, and interactions in Figma’s DevMode

- Stakeholder confidence: The founder could show the vision to potential investors and pilot customers

- User testing realism: Advisors responded to polished interfaces that felt like real software

- Design system validation: Building actual screens stress-tested Spread components

The Risk Mitigated: High-fi design can create false attachment to early concepts. I mitigated this by:

- Treating first prototypes as “directional” rather than “final”

- Maintaining a parallel low-fi sketch file for rapid exploration

- Using Figma’s component variants to maintain multiple directions simultaneously

Core User Journeys

The prototype encompassed several interconnected journeys:

1. Document Upload and AI Parsing

The Scenario: A client emails their advisor a bank statement PDF, payslips, and a partially completed paper fact-find form.

Traditional Process:

- Advisor manually reviews each document

- Transcribes relevant figures into CRM

- Cross-references to ensure consistency

- Time required: 25-40 minutes

JammJar Process:

- Advisor drags documents into upload widget

- Marvin (AI assistant) parses documents in background (2-5 minutes)

- Extracted data populates relevant fact-find fields

- Advisor reviews with “Accept” or “Edit” options

- Time required: 5-8 minutes (primarily review)

Design Patterns Introduced:

- Progressive disclosure: During parsing, show high-level progress, then reveal detailed field mappings

- Confidence visualisation: Green (high confidence), amber (medium), red (low) colour coding

- Smart defaults: Auto-accept high-confidence extractions, surface medium/low confidence for review

2. Fact-Find Management

The fact-find is the heart of mortgage advisory: a comprehensive questionnaire covering income, expenditure, assets, liabilities, credit history, and property preferences.

The Challenge: Traditional fact-finds contain 50-100+ fields. Presenting everything at once overwhelms clients; presenting too little frustrates advisors who need comprehensive data.

Our Approach: Adaptive Fact-Finding

I designed a multi-layered system:

Layer 1: Golden Questions 12 critical fields that determine basic eligibility and direction:

- Income (employed/self-employed)

- Deposit available

- Property value/purchase price

- Credit issues (Y/N)

- First-time buyer status

Layer 2: Detailed Fact-Find Complete capture across categories:

- Applicant Details

- Income & Employment

- Expenditure & Commitments

- Assets & Savings

- Property Details

- Mortgage Requirements

Layer 3: Supporting Documentation Evidence linked to specific fields (payslips to income, bank statements to expenditure)

The Interface Pattern:

- Start with Golden Questions (< 5 minutes to complete)

- AI pre-populates detailed fields from uploaded documents

- Advisor reviews and fills gaps

- System highlights incomplete sections

- Client can complete missing information via secure link

This layered approach meant clients never faced blank forms, and advisors never chased information that was already in documents.

3. Conflict Resolution

A unique challenge emerged: what happens when AI-extracted data conflicts with existing case information?

Example Scenario: Case record shows income of £45,000. New payslip upload suggests £48,000. Both might be correct (the client received a raise), or there might be an error in extraction.

Design Solution: Contextual Conflict Resolution

Rather than forcing advisors to resolve conflicts immediately (interrupting flow), we designed a notification system:

- Marvin detects conflict during document processing

- Creates notification: “Updated income information detected”

- Advisor clicks notification to see side-by-side comparison

- Advisor selects correct value or manually enters

- System asks “Why did this change?” to build audit trail

The Pattern Avoided: Early designs showed modal dialogs requiring immediate resolution. User testing revealed this created anxiety and disrupted the advisor’s work rhythm. The notification system allowed asynchronous conflict resolution on the advisor’s schedule.

4. Mortgage Product Comparison

This journey revealed the complexity beneath apparent simplicity.

The Surface Request: “Show me suitable mortgages for this client.”

The Hidden Complexity:

- 5,700+ mortgage products available in UK market

- 15+ key criteria (rate, fees, term, loan-to-value, minimum income, credit score requirements)

- Affordability calculations varying by lender

- Regulatory requirement to consider “whole market” not just preferred lenders

The Trade-off Decision:

Approach Considered: Automated Best Match AI automatically surfaces 5 “best” products based on criteria.

Approach Chosen: Guided Exploration Advisor selects 5 preferred lenders to compare, AI surfaces best product from each, advisor can adjust criteria to see how options change.

Rationale: Mortgage advisors are licensed professionals responsible for recommendations. Fully automating product selection would undermine their professional identity and potentially create regulatory risk (FCA requires advisors to demonstrate their recommendation rationale).

Instead, we designed Marvin to be a research assistant, not a decision-maker:

- Show products meeting criteria

- Highlight key differentiators

- Calculate affordability scenarios

- But: Advisor makes final product selection and documents reasoning

Interface Pattern: The Comparison Canvas

The product comparison screen used a card-based layout:

- Each lender card shows best product from that lender

- Side-by-side comparison of key criteria

- “Adjust criteria” panel updates all cards in real-time

- “Show more from [Lender]” expands to see alternative products

- “Why this product?” AI-generated summary for each recommendation

This pattern balanced efficiency (AI narrows 5,700 products to 5 relevant options) with control (advisor makes final judgment).

5. Suitability Report Generation

Every mortgage recommendation requires a Suitability Report documenting why the recommended product is appropriate for the client’s circumstances.

Traditional Process:

- Advisor uses template document (Word)

- Manually copies data from fact-find

- Writes narrative explaining rationale

- Proofreads for accuracy

- Time required: 45-90 minutes

JammJar Process:

- Advisor uploads Key Features Illustration (KFI) from lender

- Marvin generates draft report using: fact-find data, selected product details, KFI terms

- Advisor reviews in-app, can add custom commentary

- Export to PDF or Word

- Time required: 10-20 minutes (primarily review and customisation)

The Design Challenge: Trust in AI-Generated Content

Advisors were initially sceptical: “How do I know the AI hasn’t made a mistake that could cost me my license?”

Our Solution: Progressive Review Interface

The suitability report builder shows:

- Section-by-section generation: Not a single “Generate report” button, but “Generate client summary”, “Generate income analysis”, etc.

- Source highlighting: Click any figure to see source (fact-find field, KFI document, etc.)

- Editable throughout: Every sentence is editable; AI generation is starting point, not constraint

- Version comparison: “Show what changed” between AI draft and final report

The Pattern: AI as Intelligent Starting Point

Rather than position AI as producing final output, we framed it as producing a comprehensive first draft that would take advisors 30 minutes to write but 5 minutes to review and customise.

User testing validated this approach: advisors reported feeling “in control” whilst benefiting from massive time savings.

Information Architecture Decisions

The application’s overall structure emerged from card sorting exercises with advisors:

Primary Navigation:

- Dashboard (overview of all active cases)

- Cases (detailed case management)

- Clients (client database and history)

- Documents (centralised document library)

- Tasks (advisor to-do list, including Marvin-generated tasks)

- Notifications (updates, conflicts, system messages)

The Debate: Case-Centric vs. Client-Centric

Should the primary organising principle be cases (one client may have multiple mortgage applications over time) or clients (with cases nested within)?

Resolution: Case-Centric Primary, Client-Accessible Secondary

Rationale: Advisors’ daily work revolves around active applications (cases), not client histories. However, when meeting with a returning client, advisor needs quick access to previous interactions.

Implementation:

- Dashboard shows active cases

- Case detail screen includes “Client history” tab

- Client database page shows client-centric view for reference

This structure meant advisors could use the product to match their workflow (case-focused) whilst preserving access to relationship history when needed.

Bringing the Brand to Life

Parallel to product design, I developed JammJar’s brand identity. The founder had a name and a domain but no visual identity.

Brand Strategy

I created a comprehensive Brand Book modelled on Amazon’s brand documentation, including:

1. Brand Architecture How JammJar could theoretically encompass multiple products:

- JammJar Advisor (the B2B platform)

- JammJar Direct (potential future consumer offering)

- JammJar API (for integration partners)

2. Brand Positioning

- Category: AI-augmented mortgage advisory platform

- Target: Independent mortgage advisors and small firms (1-10 advisors)

- Promise: Spend 90% of your time advising, 10% on admin

- Personality: Professional but approachable, intelligent but not intimidating, innovative but trustworthy

3. Visual Identity System

I developed three distinct brand concept directions:

Concept 1: Professional Trust

- Colour palette: Navy, white, subtle green accents

- Typography: Clean sans-serif (Inter)

- Illustration style: Line-based, architectural

- Photography: Natural light, real advisors, authentic client interactions

- Tone: Confident, established, reliable

Concept 2: Innovative Energy

- Colour palette: Vibrant teal, coral accents, dark backgrounds

- Typography: Modern geometric sans (Poppins)

- Illustration style: Abstract, gradient-driven

- Photography: Dynamic, diverse, technology-forward

- Tone: Energetic, forward-thinking, disruptive

Concept 3: Human-Centred Technology

- Colour palette: Warm neutrals, soft green, touches of purple

- Typography: Humanist sans (Source Sans)

- Illustration style: Character-driven, friendly

- Photography: Candid moments, emotional connection

- Tone: Approachable, empathetic, partnership-oriented

Direction Selected: Concept 3 with Elements of Concept 1

The founder chose Concept 3’s warmth and approachability but wanted to incorporate Concept 1’s professional credibility through typography and colour balance.

![]()

![]()

![]()

![]()

![]()

![]()

Marvin: The AI Personality

One distinctive element was personifying the AI assistant as “Marvin.” This decision was strategic:

Why Personify?

- Makes AI presence less abstract and threatening

- Provides consistent “voice” for system-generated messages

- Allows for graduated capability disclosure (Marvin can “learn” new skills)

- Creates emotional connection (advisors said “Marvin found a discrepancy” not “the system flagged an error”)

Design Expression:

- Friendly icon with subtle animation (not anthropomorphised cartoon)

- Consistent visual language (Marvin’s messages use distinct styling)

- “Marvin is working…” loading states with personality

- Voice: Helpful, never condescending, occasionally playful

The Name Origin: The founder chose “Marvin” as a homage to Marvin the Paranoid Android from The Hitchhiker’s Guide to the Galaxy—an AI with immense capability but presented with personality rather than cold efficiency. (Our Marvin, thankfully, was considerably more optimistic.) Although we eventually decided not to use the name ‘Marvin’, the philosophy behind it permeated all the experiences.

Validation and Iteration

Prototype Testing with Advisors

I conducted usability testing sessions with 6 mortgage advisors (4 who participated in initial research, 2 new to the project):

Testing Scenarios:

- Upload a client document pack and review AI-extracted data

- Complete a fact-find for a hypothetical client

- Compare mortgage products and make a selection

- Generate a suitability report

Key Findings:

Success:

- Document parsing comprehension was immediate and met with genuine excitement

- Conflict resolution pattern was intuitive

- Suitability report generation inspired confidence

Iteration Required:

- Initial designs showed all uploaded documents in a single list; advisors wanted documents organised by category (income proof, ID, bank statements, etc.)

- “Accept all” button for document extraction was unused; advisors wanted to review field-by-field

- Task management felt “tacked on”; needed better integration with case workflow

Surprising Insight: Advisors valued the audit trail capability even more than time savings. One advisor said: “When the FCA audits me, being able to show where every piece of data came from and why I made each decision—that’s worth more than saving 30 minutes.”

This insight elevated compliance and traceability to first-class design considerations, not afterthoughts.

Iterative Refinements

Based on testing, I made several significant changes:

Document Organisation: Created a categorised document library with:

- Auto-categorisation (AI suggests category)

- Manual recategorisation

- “Required documents” checklist per case type

- Visual status (complete/incomplete) per category

Review Workflows: Replaced “Accept all” with:

- “Review” as default state (not requiring action)

- “Accept” button per field (explicit approval)

- “Edit” inline editing

- “Reviewed: 12/25 fields” progress indicator

Task Integration: Redesigned task management as:

- Tasks generated by Marvin in context (e.g., “Review uploaded bank statements” appears in case detail, not just task list)

- “Complete and go to next task” workflow

- Task types (document review, conflict resolution, missing information) with distinct styling

Development Handoff and Collaboration

I worked closely with Dave, the lead developer, to ensure smooth implementation.

Figma to Code Process

DevMode Usage:

- All components in Spread included detailed specifications

- Spacing, typography, colours exposed as CSS variables

- Interactive prototypes demonstrated hover states, transitions, animations

- Comments in Figma captured interaction logic and edge cases

Working in the Open: Dave and I established a collaborative rhythm:

- Daily async updates via WhatsApp and Figma comments

- Bi-weekly synchronous design reviews

- Dave built with placeholder data whilst I refined designs

- I joined Dave “in the file” to answer questions in real-time

The Advantage of Design Systems: Because Spread provided comprehensive component specifications, Dave could build features independently without waiting for pixel-perfect mocks. The system established rules; individual screens applied those rules.

Scope Management

We explicitly agreed on Phase 1 scope:

- In: Advisor platform, document upload, fact-find management, task management, notifications

- Out: Client-facing portal, mobile apps, lender API integration, advanced analytics

This clarity prevented scope creep and enabled focused delivery.

Measuring Success: The Impact Hypothesis

Whilst the product launched after my consulting period, I established success metrics during design:

Primary Metrics

Time Efficiency:

- Baseline: 90% time on admin, 10% on advisory

- Target: 50% admin, 50% advisory (Phase 1)

- Ultimate: 20% admin, 80% advisory (after full AI maturity)

Fact-Find Completion:

- Baseline: Average 2.3 advisor-client interactions to complete fact-find

- Target: 1.2 interactions (AI pre-population reduces back-and-forth)

Suitability Report Generation:

- Baseline: 60 minutes average

- Target: 15 minutes average

Secondary Metrics

Advisor Satisfaction:

- Net Promoter Score (would you recommend to fellow advisors?)

- Task satisfaction rating (1-5 scale per completed task)

Compliance Improvement:

- Completeness of audit trail

- Time to respond to FCA information requests

- Reduction in compliance errors

Qualitative Success Indicators

The Advisor Voice Shift: From: “I have to spend hours on paperwork” To: “I can focus on helping my clients make informed decisions”

The Client Experience: Even in Phase 1 (no client-facing portal), clients should experience:

- Faster response times from advisors

- More thorough fact-finding with fewer follow-up questions

- Confidence that advisor has reviewed all relevant options

Reflections: Lessons from the Journey

What Worked Exceptionally Well

1. Deep Domain Immersion Spending time in advisor offices, attending industry events, and diving into regulatory minutiae wasn’t “nice to have”—it was essential. I couldn’t design a compliance-conscious interface without understanding what the FCA actually requires.

2. Design System as Foundation Building Spread before designing product screens felt slow at the time but proved invaluable. It enabled rapid iteration, consistent handoff to development, and optionality on brand direction.

3. AI as Augmentation, Not Automation Framing AI as a tool that enhances rather than replaces professional judgment positioned JammJar as ally, not threat, to advisors. This philosophical stance shaped every interaction pattern.

4. High-Fi Prototyping for Complex Domains In a highly regulated, professional-use-case product, stakeholders (advisors, investors, regulatory experts) needed to see realistic interfaces to provide meaningful feedback. Low-fi sketches wouldn’t have elicited the depth of response needed.

What I’d Approach Differently

1. Earlier Developer Involvement Whilst Dave joined for design review, involving a technical perspective during initial concept exploration might have surfaced implementation constraints earlier, particularly around real-time AI processing expectations.

2. Quantified Workflow Analysis I documented workflows qualitatively (observation, interview) but didn’t time-study tasks rigorously enough. Having precise baseline metrics (e.g., “document data entry takes 14.2 minutes on average”) would have enabled clearer success criteria.

3. Client Research Focus on advisors was strategically correct, but I would have benefited from observing or interviewing mortgage applicants to understand their experience of the existing process. This would have informed the advisor-client interaction design more deeply.

4. Competitive Product Access I analysed competitors primarily through marketing materials and demo videos. Actually using competitor products (even if requiring sign-up under test accounts) would have revealed interaction patterns and pain points not visible externally.

The Core Insight Validated

The project validated a fundamental design philosophy: People don’t want AI to do their jobs; they want AI to eliminate the parts of their jobs that prevent them from doing what they do best.

Mortgage advisors didn’t want to be replaced by algorithms. They wanted to advise. AI’s role was to make advising possible by handling the mechanics of data management, compliance documentation, and routine analysis.

This insight should guide AI product design across domains: Don’t ask “What can AI do?” Ask “What is the human excellent at that we’re currently preventing them from doing?”

The Outcome: A Platform Poised to Transform an Industry

By April 2025, JammJar had progressed from concept to comprehensive, build-ready product:

- Spread Design System: 47 components, 12 composition patterns, 8 page templates, fully documented in Figma

- End-to-End Prototype: Clickable, high-fidelity prototype covering all primary user journeys

- Brand Identity: Complete Brand Book with visual identity system, logos, iconography, illustration, and photography direction

- Development Handoff: DevMode-ready Figma files with technical specifications

- User Stories: JTBD analysis and detailed user stories for Phase 1 implementation

- Strategic Positioning: Documented competitive analysis and differentiation strategy

The Market Opportunity Remains Immense:

- 97% of mortgage advisors report losing opportunities due to processing time (JammJar research, 2024)

- 50% time reduction in administrative tasks represents 15+ hours per advisor per month

- £1,850 average advisor monthly revenue increase from capacity to serve more clients

But Beyond Economics:

JammJar represents a vision of professional work in the AI era: humans and machines each contributing what they do best, in partnership rather than competition. Advisors retain their expertise, judgment, and interpersonal skill. AI handles the mechanics that currently bury that expertise in administrative burden.

The Hero’s Journey: Mortgage Advice Reimagined

This is ultimately a story about liberation—freeing mortgage advisors to do the work they trained for, passionate about, and excel at.

When I started this project, I spoke with an advisor named Sarah who had been in the industry for 12 years. She told me: “I went to every training course, earned every qualification, built relationships with lenders, learned the ins and outs of every niche product. And I spend my days typing into forms. It’s heartbreaking.”

Eight months later, Sarah tested the JammJar prototype. After uploading a client document pack and watching Marvin extract and populate fields, she looked up and said simply: “This is what I thought the job would be.”

That’s the measure of success: not metrics or efficiency gains, but the restoration of professional purpose.

JammJar won’t just change how mortgage advisors work. It will change what it means to be a mortgage advisor—shifting the role from data processor to trusted guide through one of life’s most significant financial decisions.

And in doing so, it will make the dream of homeownership more accessible to the thousands of people who deserve excellent, expert guidance but whose advisors currently don’t have time to provide it.

That’s the promise JammJar delivers. That’s the industry it’s changing. And that’s the future of professional work in the age of AI-augmented expertise.

This case study represents work completed between July 2024 and April 2025 as Lead Product Designer and UX Consultant for JammJar. All product designs, research insights, and strategic recommendations are the result of this consultancy engagement.

Appendices

Project artifacts

- Landing Page

- Prototype Website

- End-to-end Advisory experience

- End-to end End-user fact-find experience

- Spread Design System

- Jammjar Brand Book

Selected references

- Financial Conduct Authority (2023). Consumer Duty: Final Guidance. FCA Policy Statement PS22/9.

- UK Finance (2024). Mortgage Lending Statistics. Retrieved from ukfinance.org.uk

- Jobs to Be Done methodology: Christensen, C. M., et al. (2016). Know Your Customers’ “Jobs to Be Done”. Harvard Business Review.